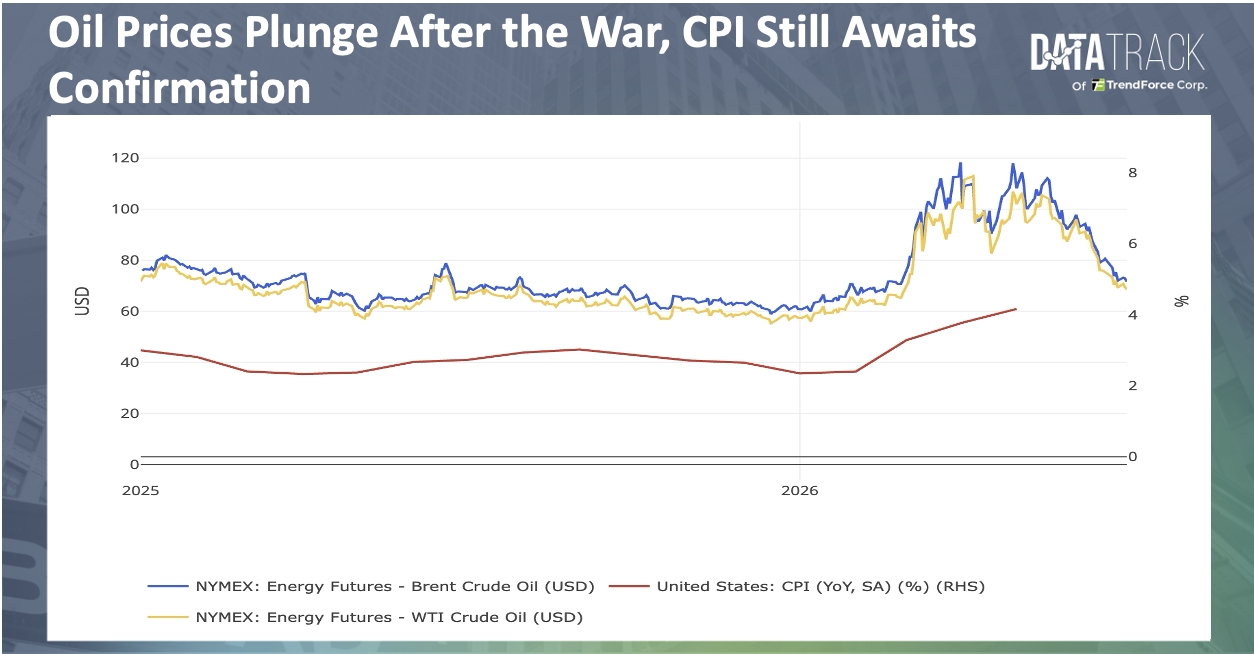

The U.S.-Iran ceasefire and subsequent progress in negotiations are rapidly reshaping the pricing logic of the crude oil market. Since mid-June, as the U.S. and Iran signed a ceasefire-related memorandum of understanding and began talks on restoring shipping through the Strait of Hormuz, the Middle East war premium that had accumulated in the market has clearly faded. International oil prices have largely returned to pre-war levels, while June saw one of the rarest monthly declines since the pandemic. As U.S.-Iran talks in Doha showed positive progress, Brent crude fell to USD 70.84 per barrel during intraday trading on July 2, while WTI crude dropped to USD 67.75, with both benchmarks extending their recent downtrend.

This decline in oil prices is crucial for the U.S. inflation outlook. U.S. CPI rose 4.2% year over year in May, with energy prices serving as a major driver of inflation and prompting markets to reprice the risk of Fed rate hikes in the second half of the year. However, as oil prices have quickly fallen from wartime highs to around USD 70, upward pressure from gasoline and energy costs on CPI and PCE is expected to gradually ease. If oil prices remain in the current range, May could very likely mark the inflation peak of this round of geopolitical shock, while the urgency for the Fed to resume rate hikes would also be significantly lower than before the June meeting.

Still, current market pricing reflects an optimistic scenario of an extended ceasefire, restored shipping, and normalized supply, while the repair of physical supply chains will take time. Although shipping through the Strait of Hormuz is gradually resuming, risks related to mines, shipping insurance costs, designated shipping routes, and vessel safety assessments will continue to limit the speed of recovery. Iran has also recently insisted on retaining influence over traffic management in the Strait of Hormuz, and may even seek to strengthen control through fees or route restrictions in the future. This makes it difficult for markets to fully price out the Middle East risk premium. From a supply-demand perspective, low inventories and restocking demand may also limit further downside in oil prices. During the earlier Middle East conflict, some countries stabilized energy supply by releasing commercial inventories and strategic reserves. Now that oil prices have fallen, importers and refiners may instead restart restocking. This means that although oil prices are under pressure in the short term from the fading war premium, they may still find support at lower levels if restocking demand rises, OPEC+ increases output by less than expected, or another security incident occurs in the Strait of Hormuz.

Looking ahead, oil prices will remain a core variable in determining whether U.S. inflation has truly peaked. If the Doha talks continue to advance and the normalization of Persian Gulf crude oil and LNG exports is confirmed, energy prices will help lower inflation readings after June and expand the Fed’s room to keep rates unchanged. However, the U.S.-Iran ceasefire has only shifted crude oil pricing from a “wartime supply shock” back toward supply-demand fundamentals; it does not mean inflationary pressure has fully disappeared. Markets still need to watch three key risks: whether U.S.-Iran talks can move from a temporary ceasefire to a more stable agreement; whether traffic through the Strait of Hormuz can truly return to pre-war levels; and whether global restocking demand under low inventory conditions pushes oil prices higher again. For the Fed, lower oil prices provide temporary breathing room. For markets, the real question is whether energy prices can remain stably low, rather than merely giving back the war premium temporarily.